"We Sell Stuff Nobody Really Needs"

"We Sell Stuff Nobody Really Needs"

A preview of my deep dive on Five Below

Thank you for signing up for the TSOH Investment Research Service. My goal with these emails is to give you a sense for the quality of research being delivered to paid subscribers. If there’s anything I can do to help you learn about the service or to see if it would be additive to your investment process, reach out anytime (DM or thescienceofhitting@gmail.com)

This morning, I emailed subscribers a research report on Five Below (FIVE), a company that has increased revenues at a 26% CAGR over the past decade. This email includes a preview of the write-up. If you’re interested in learning more, please sign-up for the TSOH Investment Research Service.

Five Below (FIVE) is a U.S. retailer that focuses on selling products for $5 or less to the roughly 63 million people aged 5 to 19 in the country (teens and tweens). The average Five Below carries roughly 4,000 SKU’s in a 9,000 square foot box within high-traffic shopping centers (management estimates that about half of their store traffic is attributable to customers who were in the shopping center to visit a co-tenant like TJ Maxx, Marshalls, or Ross).

Five Below meets one of my key criteria for a retailer - it’s Amazon-proof. The reason why is the nature of the transaction: the average customer spends about $150 a year at Five Below, buying ~60 items over the course of ~10 trips to the retailer. That implies six items purchased per visit for about $15 (an average cost of $2.50 per item – think novelty socks, seasonal products, art supplies, a cheap basketball, candy, etc.). I believe the company has cover from e-commerce risk due to the low-dollar value of its average transaction and the unplanned / impulsive nature of the purchase decision (“You don’t go into the store knowing you want a selfie stick, a mug in the shape of the smiling turd emoji and lip gloss”); the company’s own lackluster e-commerce efforts, at <$100 million in annual sales five years after launch, speaks to this reality (“shipping often costs more than the entire purchase”).

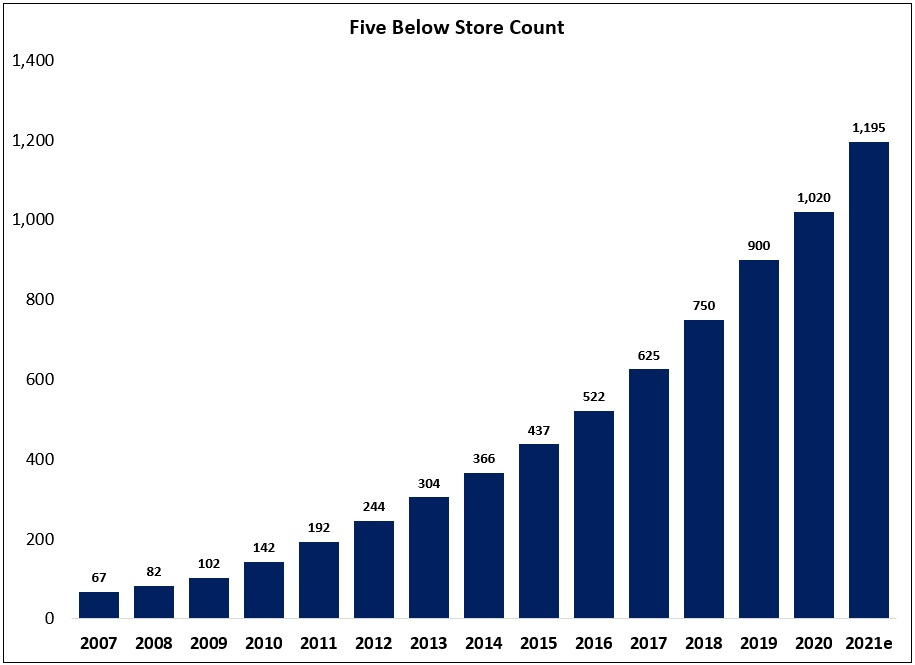

This is still a relatively new concept: Five Below opened its first store near Philadelphia in 2002 (IPO in July 2012). Over the course of the next 18 years, the footprint expanded to more than 1,000 locations across 38 states, with plans to add another 170 - 180 stores throughout 2021 (funded through retained earnings; the company ended FY20 with $410 million in cash on its balance sheet and no debt). Long-term, management believes there’s an opportunity for more than 2,500 Five Below stores in the United States.

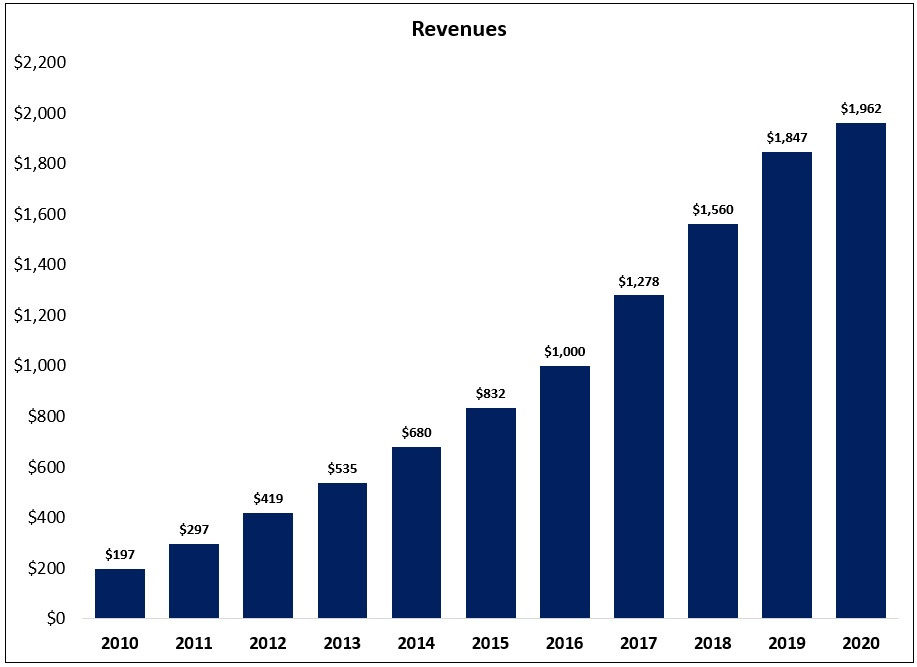

Revenues have followed suit: over the past decade, Five Below’s annual revenues have increased ten-fold to nearly $2 billion a year (26% CAGR).

In 2019, co-founder Thomas Vellios spoke about the original business plan:

“We knew there was a ton of money being spent by this universe of kids, but nobody was really creating something new… You had about $24 billion being spent in the toy sector every year. But then we realized that kids, by the time they got to the age of 5 or 6, we’re exiting the toy stores… toy stores didn’t evolve. So, once you got to that age, you no longer stayed in toy stores… And the biggest toy store in America [Toys R Us] never really figured out how to sell to kids. It was the most unfriendly store… some bike or some big box from 12 feet up could fall and crush you. So, that was a good thing for us.

Then we looked at kids aged 13, 14, and over… all going to the mall, “mall rats”. And then there was a segment in the middle… “tweens”, nobody really went after that segment. Affordability was key if you wanted to create a business that was universal in appeal. It didn’t matter how much money you had; you were able to afford Five Below. We looked at dollar stores, but we really didn’t like them for kids – yes, you go there and you shop, but they were dirty (at least at the time)… they were more of a needs based store, you bought a roll of Charmin toilet paper for $1. That wasn’t our gig.

So, we wanted to recreate a store that was magical to me growing up when I came to the U.S. In those days, they had stores called five and dimes… was there a space to create a new approach to a modern day five and dime? A store kids would call their own. But, at the same time, that moms would approve… When we looked at the dollars spent in a given year for this group – both by the kids and the parents – it was in excess of $200 billion.

So, needless to say, the landscape was ripe for disruption.”

That business plan and target audience led to a number of “must haves” for Five Below. First, the assortment had to be “trend right” (as Mr. Vellios notes, “we sell discretionary goods; in layman terms, we sell stuff nobody really needs – and we want you to buy it all the time”). Second, unlike the towering racks of bikes and boxes at Toys R Us, Five Below aspired to create a store environment that was attractive to its target customer (“easy to navigate, sight lines across the entire store, cool and vibrant colors, great music playing”). And third, product affordability was a major focus for the founders - and when your core shopper relies on a $20 weekly allowance from their parents as their sole source of “income”, that meant selling products for $5 or less.

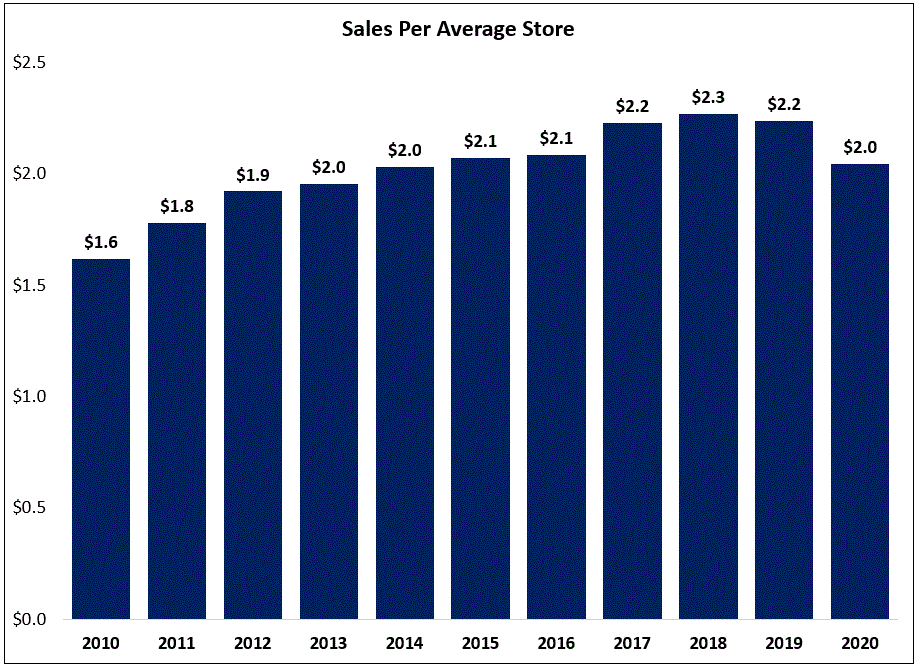

Despite a growing store base, unit economics have continued to improve over the years: as shown below, the average Five Below generated roughly $2.2 million in revenues in 2019 – about 40% higher than at the start of the decade (the company faced pandemic-related headwinds in 1H 2020, including the closure of all stores throughout most of March and April).

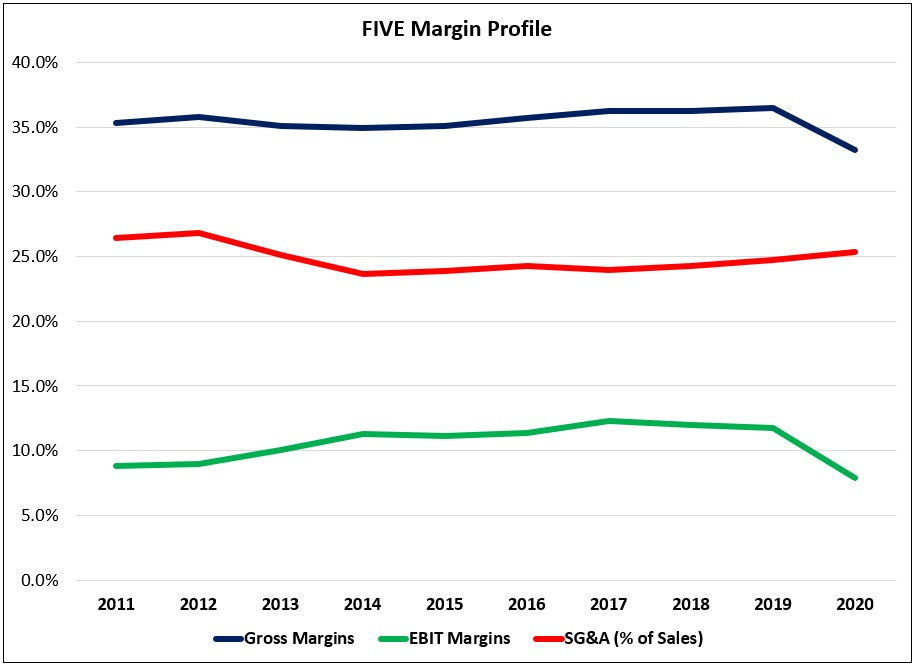

In addition, the unit economics are very attractive: using 2017 - 2019 average EBIT margins of ~12% (shown below), a typical Five Below generates about $265,000 in operating income per year. To put that number into context, the average Dollar Tree - another retail banner that I love - generates about $220,000 in operating income on $1.7 million in sales (~13% margin).

If there’s anything that concerns me in the recent results, it’s traffic trends…

(End of Preview)

NOTE - This is not investment advice. Do your own due diligence. I make no representation, warranty or undertaking, express or implied, as to the accuracy, reliability, completeness, or reasonableness of the information contained in this report. Any assumptions, opinions and estimates expressed in this report constitute my judgment as of the date thereof and is subject to change without notice. Any projections contained in the report are based on a number of assumptions as to market conditions. There is no guarantee that projected outcomes will be achieved. The TSOH Investment Research Service is not acting as your financial advisor or in any fiduciary capacity.